AML Rules on Virtual Basketball: Why Source-of-Funds Checks Hit High-Frequency Play Hardest

The Email That Stopped a Withdrawal in Its Tracks

A friend of mine had what he thought was a routine month on virtual basketball – nothing dramatic, just steady play across forty or fifty sessions that ended marginally up. When he requested a withdrawal of £600, the operator’s automated system held the request and sent him an email asking for three months of payslips and a bank statement. He thought it was a scam. It was not. It was the operator’s anti-money-laundering source-of-funds check kicking in, exactly as UK regulation requires, on a customer profile that the operator’s risk model had flagged as warranting verification.

The AML regime on virtual basketball is the most underappreciated piece of the regulatory architecture from the customer’s perspective. It also kicks in at activity levels that surprise punters who think of themselves as low-stakes recreational players. The cycle speed of virtual basketball makes the AML thresholds easier to cross than they look on slower products, and understanding why the system works the way it does helps avoid the friction it creates.

Why Gambling Sits Inside the AML Framework

The UK’s anti-money-laundering framework treats gambling operators as designated reporting entities under the Money Laundering Regulations 2017 (as amended). The designation requires gambling operators to apply customer due diligence, monitor transactions for suspicious activity, file Suspicious Activity Reports to the National Crime Agency when warranted, and maintain records that can support investigation if criminal proceeds are suspected to be flowing through the operator’s platform.

The logic for including gambling in the AML framework is that the sector has historically been used to launder criminal proceeds. Cash-rich businesses, products that allow rapid conversion of funds into different forms, customer bases with limited identity verification – these are the structural features that made unregulated gambling attractive to launderers, and the regulatory framework is designed to close those routes. The UK’s gambling licensing regime, which requires KYC verification before play and source-of-funds verification at higher activity levels, is the front line of that closure.

Virtual basketball sits inside the framework with no carve-out. The product’s RNG-driven nature does not exempt it from AML rules – if anything, the cycle speed makes it a higher AML risk than slower products because the volume of transactions across a short period is large and the per-transaction sums are typically small enough to fall below superficial scrutiny. The aggregate is what triggers the checks, not the individual bets.

The Risk Model That Triggers Checks

Every UK-licensed operator must maintain a risk model that defines the activity thresholds at which enhanced due diligence kicks in. The model is operator-specific and confidential – the regulator does not publish a standard threshold because doing so would help bad actors structure their activity to stay just under the line – but the general shape of the model is well-understood across the industry.

The factors that typically feed the model include cumulative deposit volume over various time windows, net loss patterns relative to deposit volume, deposit source diversity (number of payment methods used), withdrawal patterns, the relationship between the customer’s verified income profile and their gambling activity, and behavioural indicators like session frequency and timing. Each operator weights these factors differently, but the broad result is that customers whose activity exceeds normal recreational levels get flagged for additional verification.

The thresholds activate earlier than most punters expect. A virtual basketball player who places 100 bets at £2 across a fortnight has generated £200 of stake turnover with relatively low net loss, but the activity pattern – frequent small bets, fast cycles, multi-session weeks – fits the risk profile that the model treats as warranting enhanced due diligence at fairly modest absolute amounts. The exact figure varies by operator, but customers should expect source-of-funds requests at total deposit levels well below typical UK monthly incomes.

What Source-of-Funds Verification Looks Like

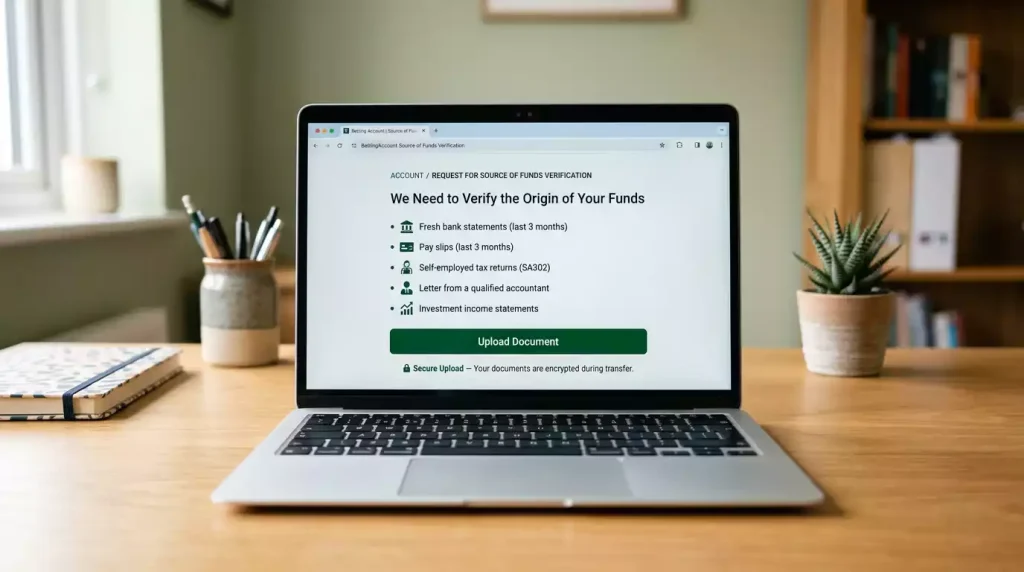

The operator’s source-of-funds request typically asks for documentation showing the legitimate origin of the funds being gambled. The accepted documents vary by case but commonly include: recent payslips showing employment income, bank statements showing salary credits and overall account behaviour, employment confirmation letters, tax returns or HMRC correspondence, pension statements for retirees, and evidence of business income for self-employed customers.

The bar for sufficiency is that the documentation must demonstrate the funds being gambled are consistent with the customer’s legitimate income profile. A customer with £2,500 monthly salary credits showing on bank statements who is depositing £300 a month on virtual basketball produces a clean picture. A customer with no obvious income source on the statements who is depositing £1,200 a month requires additional explanation. The operator’s reviewer makes the affordability judgment based on the documentation submitted.

The verification typically takes a few business days to complete once the customer has uploaded the requested documents, with the customer’s account effectively frozen for further deposits and withdrawals during the review. Bet365, Sky Bet and other major operators have built relatively streamlined upload portals that handle the document collection and review, but the review itself remains substantively a human task at most operators because the affordability judgment requires interpretation rather than rule application.

The Affordability Check Layer

Source-of-funds verification overlaps with a related framework called affordability checks, which the UKGC requires operators to apply alongside the AML regime. Affordability checks are not strictly an AML mechanism – they exist primarily to enforce the LCCP’s harm prevention provisions – but they use the same documentation and operate on similar thresholds, so customers experience them as part of the same regulatory friction.

The affordability framework asks a slightly different question than the AML framework. AML asks: is this money the customer’s legitimately earned funds? Affordability asks: can the customer afford to lose this money without harm? A customer with a clean source-of-funds profile but very limited disposable income relative to their gambling activity can fail an affordability check even if they pass the AML test. The operator must then either reduce the customer’s deposit capacity, increase the documentation requirements, or in some cases impose enhanced monitoring on the account.

The framework is contested at the policy level. Grainne Hurst, the CEO of the Betting and Gaming Council, framed the industry concerns about over-broad affordability application: “Massive tax increases for online betting and gaming announced in the Budget make them among the highest in the world, and are a devastating hammer blow to tens of thousands of people working in the industry across the UK.” The affordability checks are one of several mechanisms that industry has argued are pushing customers toward unlicensed alternatives, with illegal gambling stakes in the UK rising from roughly £5 billion in 2019 to around £16.6 billion in 2025 according to H2 Gambling Capital research. The policy balance between consumer protection and licensed market viability is one of the active debates in UK gambling regulation.

What Customers Can Do to Smooth the Process

The friction of AML and affordability checks is reducible but not eliminable. Customers who anticipate the verification can take several steps to make it smoother when it arrives. Maintaining current and accessible income documentation – recent payslips, current bank statements showing salary credits, employment confirmation – means the document upload can happen quickly when requested. Using a single deposit method consistently produces a cleaner pattern for the operator’s risk model than rotating across multiple methods.

Setting a deposit limit before the verification trigger activates is the cleanest preventative step. A customer whose monthly deposit cap is set at £300 will rarely trigger source-of-funds verification at most operators, because the cap keeps the activity pattern below the typical risk threshold. The same customer with no cap who happens to have a heavier month might cross the threshold and find their next withdrawal held pending documentation. The cap is the simplest way to keep the AML regime out of the casual recreational experience.

Maintaining consistent activity levels also helps. A customer who places £50 of bets every week for a year produces a stable pattern that the operator’s risk model can read clearly. A customer who places £2 of bets for ten months then suddenly places £500 in a single week produces an activity spike that almost always triggers verification regardless of the absolute amounts involved. The model is looking for changes in pattern as much as for crossing of absolute thresholds.

What the System Looks Like From the Regulator’s Side

From the UK Gambling Commission’s perspective, the AML and affordability frameworks are mutually reinforcing components of a single regulatory programme. Andrew Rhodes, the Commission’s CEO, captured the enforcement intensification in his ICE 2025 keynote: “Year on year we saw a 300 per cent increase in the number of criminal cases we were taking as a regulator.” The intensification covers both unlicensed operators bypassing the regime entirely and licensed operators failing to apply the regime effectively. Both routes lead to regulatory action.

The system has visible effects beyond individual customer experiences. The Health Survey for England has found that 18.2% of online gamblers are at-risk or problem gamblers compared with 5.8% of all gamblers, and the AML/affordability framework is one of the structural mechanisms that catches the higher-risk customers before their activity escalates. The 77.6% share of the global virtual sports market held by RNG-driven products in 2025 sits across a customer base where this structural catchment matters, and the UK’s framework is widely regarded internationally as the most comprehensive in the regulated space.

For the punter, the implication is that the friction of the AML regime is the cost of operating inside a licensed framework that provides serious protections in return. Unlicensed alternatives skip the verification but also skip the consumer protections, the dispute resolution access, the segregated customer funds, and the certified fairness regime that gives the licensed product its actual value. The five-minute upload of a payslip is a small price for the architecture sitting behind it. For more on the broader regulatory context this verification sits inside, my piece on virtual basketball age verification covers the entry-level KYC framework that sits alongside the AML regime.

Why am I being asked for source-of-funds documentation when I have already verified my identity?

Identity verification and source-of-funds verification are separate regulatory requirements at different activity thresholds. Identity verification happens at account opening to confirm who you are and that you are old enough to gamble. Source-of-funds verification happens at higher activity levels to confirm that the funds being gambled come from legitimate sources, under both the Money Laundering Regulations and the LCCP"s affordability framework. Both checks are mandatory under UK regulation when their respective triggers activate.

What happens to my account if I refuse to provide source-of-funds documents?

The operator"s system will keep the account locked for further deposits and withdrawals until the documentation is provided. The customer"s existing balance remains theirs but cannot be played or withdrawn during the lock. If the customer ultimately refuses to provide the documentation, the operator typically closes the account and returns the balance to the original payment source. The operator is not allowed to release the funds or allow continued play without completing the verification, because doing so would be a regulatory breach on the operator"s side.

Articles

Created by the "Virtual Basketball Bet" editorial team.